Some Known Questions About Mortgage Investment Corporation.

Some Known Questions About Mortgage Investment Corporation.

Blog Article

The Buzz on Mortgage Investment Corporation

Table of ContentsGet This Report on Mortgage Investment CorporationEverything about Mortgage Investment CorporationThe Best Strategy To Use For Mortgage Investment CorporationExamine This Report about Mortgage Investment CorporationThe Facts About Mortgage Investment Corporation Uncovered

Does the MICs credit scores board review each home mortgage? In most situations, home loan brokers handle MICs. The broker needs to not work as a participant of the credit history board, as this places him/her in a straight problem of interest given that brokers typically make a compensation for positioning the mortgages. 3. Do the directors, members of credit scores committee and fund manager have their own funds invested? Although an indeed to this inquiry does not offer a risk-free financial investment, it must give some raised security if evaluated combined with other prudent lending policies.Is the MIC levered? The economic establishment will approve certain home loans owned by the MIC as safety and security for a line of credit report.

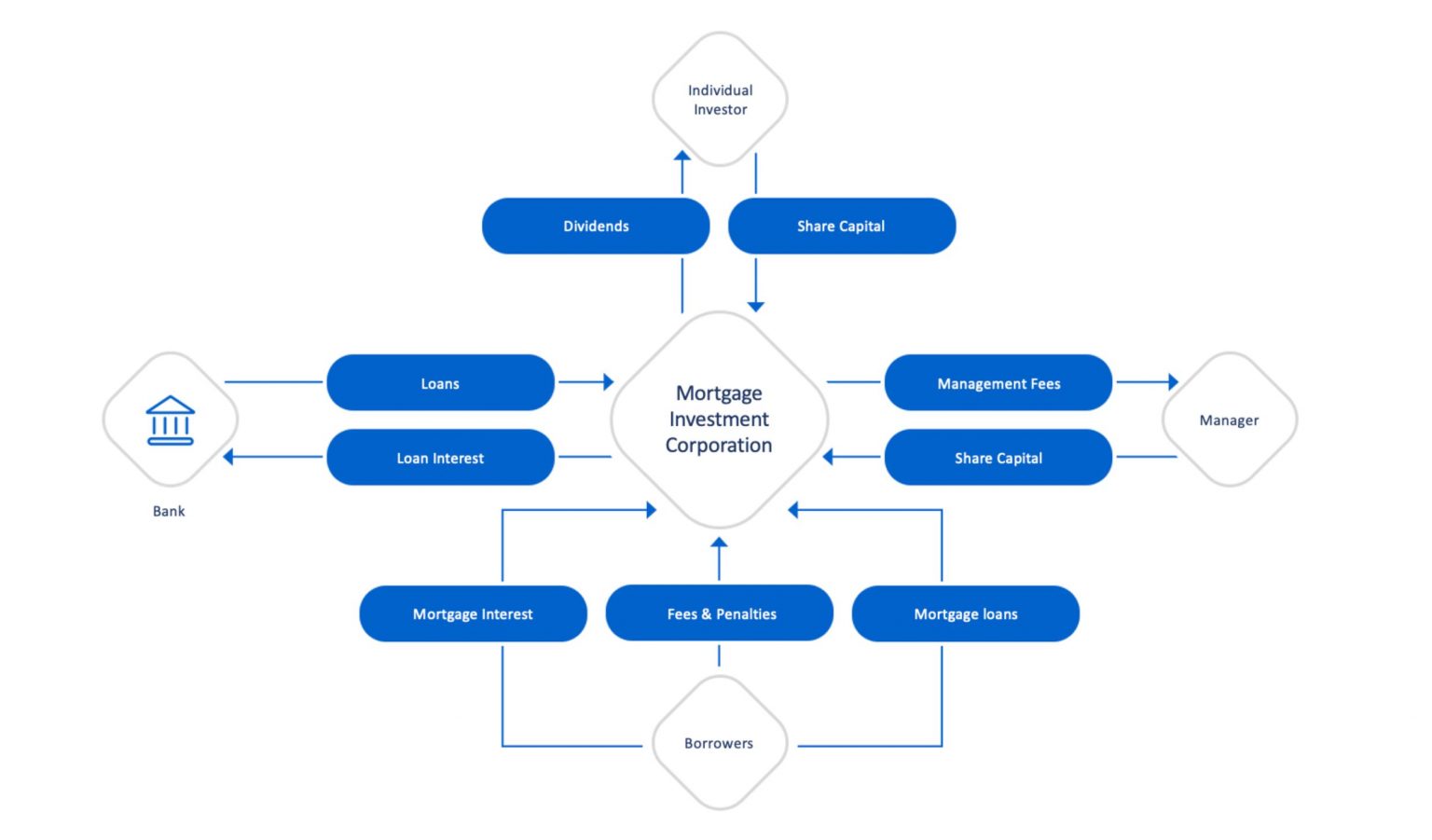

Last upgraded: Nov. 14, 2018 Couple of financial investments are as beneficial as a Mortgage Financial Investment Corporation (MIC), when it concerns returns and tax advantages. Due to their corporate framework, MICs do not pay income tax obligation and are lawfully mandated to disperse all of their earnings to investors. In addition to that, MIC returns payouts are dealt with as interest revenue for tax purposes.

This does not indicate there are not dangers, yet, typically speaking, regardless of what the more comprehensive stock exchange is doing, the Canadian property market, especially significant cities like Toronto, Vancouver, and Montreal performs well. A MIC is a corporation formed under the guidelines lay out in the Earnings Tax Obligation Act, Section 130.1.

The MIC earns income from those mortgages on passion costs and basic charges. The genuine charm of a Home loan Financial Investment Corporation is the return it gives capitalists contrasted to other fixed earnings investments - Mortgage Investment Corporation. You will have no problem locating a GIC that pays 2% for an one-year term, as government bonds are equally as low

Mortgage Investment Corporation - The Facts

A MIC has to be a Canadian firm and it should spend its funds in home loans. That claimed, there are times when the MIC finishes up having the mortgaged residential or commercial property due to repossession, sale agreement, etc.

MICs issue usual and favored shares, issuing redeemable recommended shares to shareholders with a dealt with returns price. These shares are considered to be "certified financial investments" for deferred earnings strategies. This is excellent for read this post here financiers that purchase Home loan Investment Corporation shares with a self-directed registered retirement financial savings plan (RRSP), registered retirement revenue fund (RRIF), tax-free savings account (TFSA), delayed profit-sharing strategy (DPSP), registered education cost savings strategy (RESP), or registered handicap savings plan (RDSP)

Not known Details About Mortgage Investment Corporation

And Deferred Plans do not pay any type of tax obligation on the rate of interest they are approximated to get. That claimed, those who hold TFSAs check and annuitants of RRSPs or RRIFs might be struck with specific fine taxes if the investment in the MIC is taken into consideration to be a "banned investment" according to Canada's tax code.

They will ensure you have actually located a Mortgage Investment Corporation with "professional investment" condition. If the MIC certifies, maybe really useful come tax time because the MIC does not pay tax on the passion earnings and neither does the Deferred Strategy. Much more generally, if the MIC falls short to meet the demands laid out by the Earnings Tax Act, the MICs revenue will be tired prior to it obtains dispersed to investors, lowering returns considerably.

Several of these threats can be reduced though by speaking with a tax expert and investment rep. FBC has actually functioned solely with Canadian local business proprietors, business owners, investors, ranch operators, and independent professionals for over 65 years. Over that time, we have actually helped 10s of thousands of customers from throughout the country prepare and file their tax obligations.

The Buzz on Mortgage Investment Corporation

It shows up both the genuine estate and stock markets in Canada are at all time highs Meanwhile returns on bonds and GICs are still near document lows. Even cash is losing its appeal since energy and food rates have pressed the rising cost of living price to a multi-year high.

If passion prices climb, a MIC's return would certainly additionally raise because see greater home loan rates imply even more revenue! MIC capitalists simply make money from the enviable placement of being a lender!

Numerous effort Canadians that intend to get a residence can not obtain home mortgages from traditional banks since maybe they're self employed, or don't have a well-known credit scores history yet. Or maybe they desire a short term finance to develop a large building or make some improvements. Banks have a tendency to disregard these potential debtors because self employed Canadians don't have secure revenues.

Report this page